Fund firms warned of industry revenue shift

Few asset managers are aligning to the future revenue opportunities in Asia Pacific, warns consultancy Casey Quirk* – namely insurance companies, retail investors, regional private banks and defined-contribution pension schemes.

The firm forecasts the market share of these segments will rise to 58% of regional assets under management by 2018, from 36% in 2013. It argues sovereigns, large pension schemes and global private banks – the previous buyer preferences – represent a shrinking share of opportunity.

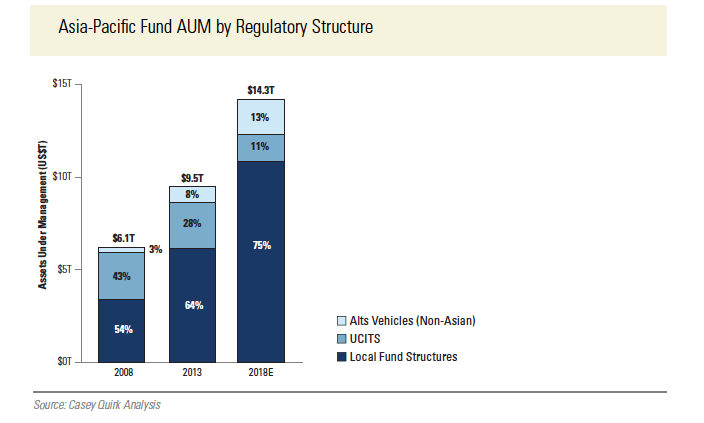

Casey Quirk notes, too, that Ucits platforms designed for other geographies will continue to see their share of Asia-Pacific fund AUM erode, from 28% in 2013 to 11% by 2018 – in other words, more than halved.

The research shows that Asia-Pacific asset management revenues grew twice as fast as those in Europe and North America between 2009 and 2013.

But Casey Quirk is suggesting managers need a new playbook, and points to changing buyer demographics.

Historically sovereign funds, large national pension systems, global private banks, Japanese retail investors and Australia’s superannuation system have driven growth in Asia-Pacific revenues. These segments accounted for the majority of industry AUM at the end of 2013 (see chart).

But the consultancy predicts that another group – local retail and private banks, Aussie self-managed supers, insurers, DB pensions, DC pensions and IFAs/family offices – will account for almost 60% of revenues in the region by the end of 2018.

This it bases on three premises:

- Larger asset owners are now well covered by managers and consultants and represent lower-margin prospects. While more fragmented segments may be costlier to address, fewer competitors have invested in them and fee pressure has not fully materialised.

- Large asset owners are beginning to manage more of their own assets. Conversely rising segments such as local retail banks lack the size to pay for internal asset management skills, and are increasingly seeking help from external asset managers, both global and local

- Regional regulators have applied pressure to national pension systems, and are encouraging growth in rising segments and new capital pools, such as locally domiciled DC schemes.

Casey Quirk also points to evolving product demand in Asia Pacific. Since 2009, alternative investments, global and regional portfolios and multi-asset propositions have gained share at the expense of domestic, single-country and long-only equity and bond portfolios (see chart).

While locally focused strategies still represent half the region’s AUM, they only account for 20% of the local industry’s net revenues.

The consultancy also highlights the steady erosion of Asia-Pacific fund assets domiciled outside the region, particularly into European Ucits structures, which it forecasts will see its share of regional assets drop precipitously.

Trends encouraging a shift to locally domiciled funds include regulatory drivers from proposed fund passporting and changing buyer preferences.

“A clear conclusion is that global managers should not count on Asia-Pacific assets to help amortise the costs of a large Ucits platform in Europe,” Casey Quirk notes in its report.

“On the other hand, an eventual Asian passport, crucially one that includes the mainland Chinese market, has better chances of success, largely because it will promote managers with locally based product development and management functions.”

* Casey Quirk has published its forecasts and views in a new report, Evolving Markets: A Practical Framework for Asset Management in Asia Pacific.